Going beyond the buzz word

If you consume financial news, chances are you have heard the term “FinTech” (a lot). There is no doubt; FinTech is a buzzword. Just three short years ago circa 2014, there was very limited discussion around the topic. Now, it is regularly splashed across mainstream media headlines. One need not look far for evidence as a simple search in Google Analytics reveals the mounting FinTech tsunami.

I want to go beyond the hype to form a deeper understanding of what is driving the wave of FinTech, because it is fundamentally different than past innovation in financial services. It is driven by fundamental changes which have shifted power from established firms to new entrants, it unites a range of sub-themes, and most importantly, it opens the door to convergence with other industries.

Fintech 101

What we often hear consistently from newcomers to FinTech is that it is nothing new with technology having enhanced financial services since the beginning. High frequency trading is the same basic concept behind carrier pigeons – reducing latency to create value. We all saw ATMs and used online banking before FinTech became popular. So, it is fair to ask, why are we talking about something different now?

Firstly, it is important to note that FinTech emerged just a few years after the global financial crisis, which most attribute to financial innovations like mortgage backed securities and credit default swaps. This was a turning point whereby traditional financial centers started to erode and FinTech hubs began to emerge. It was out of the ruins of financial engineering that a new type of innovation was sought – an innovation which better serves consumers. A perfect example of this is the crypto currency movement, which in many ways traces its roots to Occupy Wall Street.

Secondly, two technological enablers shifted the balance of power from established firms to new entrants: ultra-low-cost computing and mobile. Established financial services players are burdened with legacy businesses and have struggled to exploit new opportunities to reinvent their business models; whereas, new entrants have shown they are driving the introduction of new business models and adapting to clients’ new expectations.

Because of these two trends, FinTech is much more than the typical relationship of technology enhancing financial services. We are witnessing the digital transformation of financial services and introduction of previously unseen business models by new entrants.

FinTech pulls together related topics

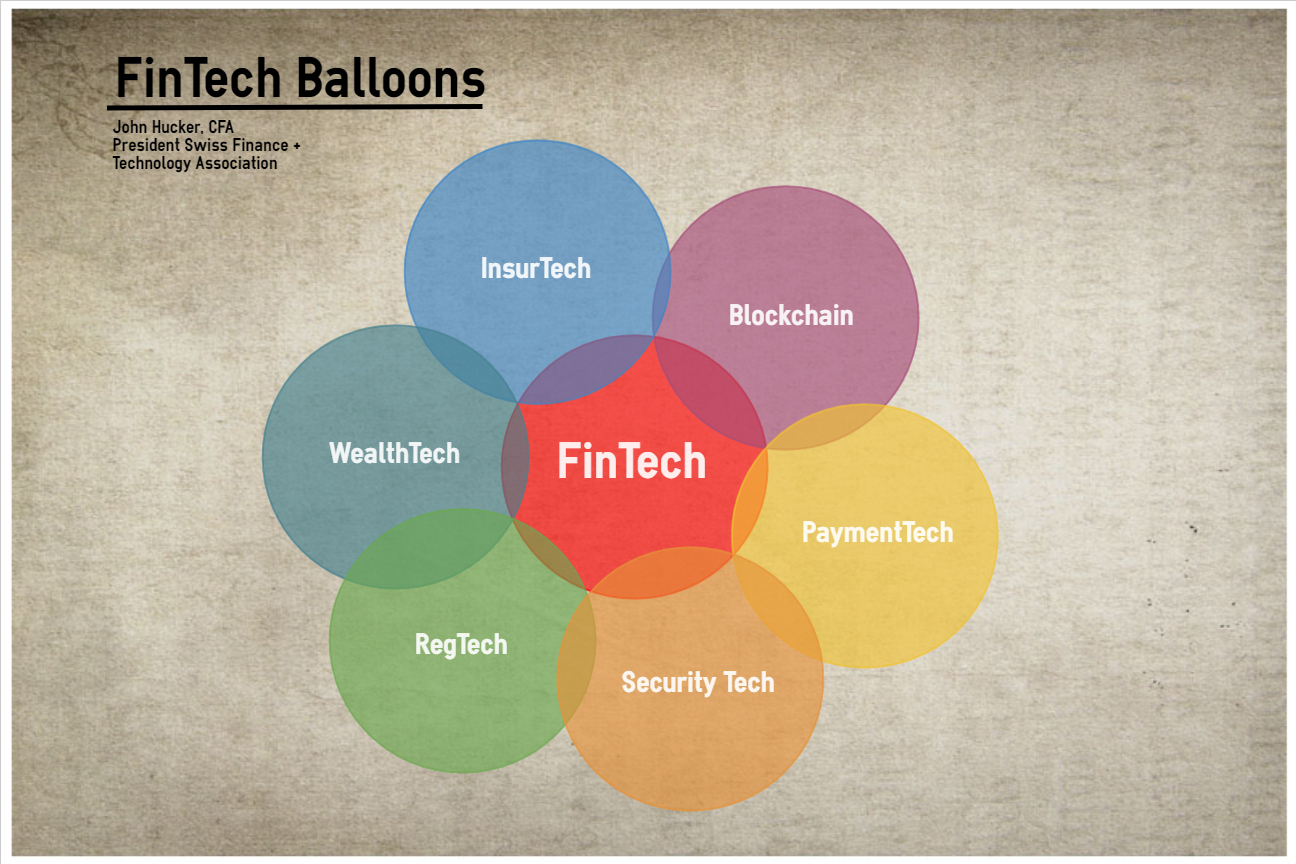

FinTech does not apply to banking alone, nor is it a simple catch-all phrase or umbrella statement. FinTech is the common bond between several related themes, which also have unique distinctions. FinTech is what connects Blockchain and WealthTech, or InsurTech and RegTech. They are separate topics which each demand their own focus and, in some cases, they go well beyond traditional financial services. For example, InsurTech may overlap with WealthTech when it comes to robo-advisors, but then goes in a separate way to look at autonomous cards, IoT, and other areas which have little to do with banking. Similarly, Blockchain may have started with bitcoin and payments, but it extends well beyond finance into various applications or contracts and decentralized systems.

While some argue these are separate topics, we see huge synergies. Accordingly, our Association focuses its center of gravity to connect with existing specialized partners and expand into adjacent areas.

FinTech+

There is a growing trend to flip from FinTech to TechFin. This highlights that technology players (i.e. Uber, Alibaba, Amazon, Tencent) are adding finance as a layer to their core business and distributing to their current customers. There is more to it than whether finance or technology takes the lead position.

It was mentioned that + is used to indicate convergence. At the surface, this speaks to the blending of finance + technology, but it extends deeper to offer a unique opportunity for Switzerland. FinTech is converging with other industries, from life sciences, health to travel and many more. Few other locations in the world are so well positioned as Switzerland to play a leading role in this convergence. Not only are global leaders in many industries present, Switzerland offers the ideal setting for corporate innovation management with its strong legal frameworks, tax efficiency, attractiveness for skilled workers, and innovative culture.

Final words

Switzerland has the chance to become a global hub for corporate innovation and FinTech+ is at its core. To reach its potential, Switzerland must catch up in terms of its appreciation for the nuances of the FinTech opportunity. It must foster a more cohesive FinTech ecosystem including Blockchain, RegTech, InsurTech, and other relevant areas. And finally, it must look beyond the current hype of mainstream FinTech to seize the huge potential of convergence across industries with FinTech at the core. More will be said about how exactly to do this in future posts.

Article written by John Hucker, CFA, MBA (Twitter | LinkedIn)