Written by Georgi Zai

In a previous article (How people perceive value in Financial Services) we focused on Reference Point Dependence, and how crucial it is for understanding how people perceive value. In this article, we dive into Loss Aversion, another important principle that provides valuable insights for crafting a strong value proposition.

The emotional weight of loss

If Reference Point Dependence provides the baseline for assessing value, then Loss Aversion governs the intensity of emotional reactions to losses and gains.

Unlike utility theory, which suggests a linear, symmetrical impact of gains and losses, prospect theory reveals an emotional asymmetry: losses generally exert a greater psychological impact than equivalent gains.

Hence Loss Aversion establishes a unique emotional asymmetry in value perception that companies cannot afford to overlook!

In simpler terms, humans tend to experience a loss of $100 as twice as emotionally painful as the pleasure derived from gaining the same amount. This emotional asymmetry holds true for both monetary and non-monetary domains. It presents both a challenge and an opportunity for shaping and fine-tuning a value proposition.

Striving on the concept of avoiding losses

Following the concept of Loss Aversion, businesses must attempt to eliminate or minimize aspects of their offerings that could be perceived as losses. In the best case scenario, they can leverage this effect by introducing features that assist customers in avoiding losses in other products or life situations.

For instance, the absence of a banking license in a fintech firm might be seen as a glaring shortcoming, potentially overshadowing other merits of its offering for some customers. Companies must be keenly aware and agile in addressing such shortcomings. In the best case scenario, they can leverage this effect by introducing features that assist customers in avoiding losses in other products or life situations.

To illustrate the last point, let’s examine Stripe, a key player in the payment solutions landscape. Stripe’s approach builds directly on the principle of Loss Aversion, offering a set of features that, among others, minimize potential customer losses. These include Stripe Radar, chargeback protection, and real-time transaction monitoring.

Harnessing and challenging ownership (endowment effect)

Next, we will explore the Endowment Effect, which arises as a consequence of Loss Aversion. This psychological mechanism instills a powerful sense of ownership, making the thought of “letting go” feel like a loss.

For instance, consider the appeal of free accounts offered by payment services such as Revolut. While these accounts provide a limited set of services, merely owning such an account increases its perceived value. This emotional connection not only ensures user retention but also creates an opportunity for effective upselling, whether through value-added services or fees. Free-tier accounts, trial periods, and customization activate the Endowment Effect.

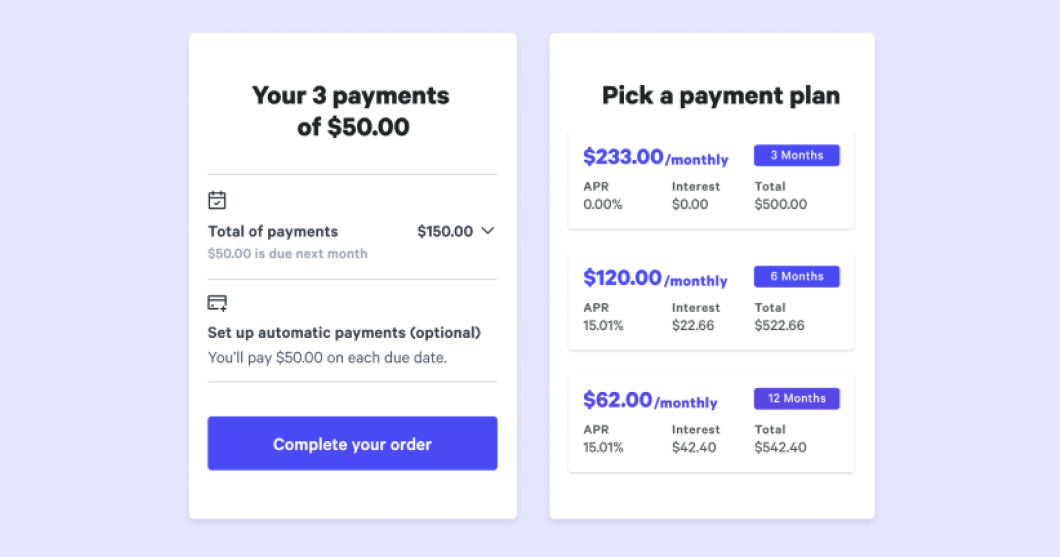

The sense of ownership can also extend beyond product trials or freebies. Customization options, such as those found in BNPL solutions like Affirm, add another layer of psychological ownership. Allowing customers to tailor their payment schedules not only adds convenience, but also subtly reinforces their commitment to the service.

When used intelligently, this technique can even help overcome certain drawbacks of an offering. For example, SoFi engages its users through personalized events, webinars, and tailored financial advice. This strategy creates a sense of belonging and ownership among customers, making them less concerned with interest rates or fees.

The weight of past investment (sunk cost fallacy)

Lastly, let’s examine the Sunk Cost Fallacy, another cognitive bias that explains why people may be reluctant to adopting innovations. It compels people to continue with an activity or commitment, regardless of the current or future value, simply because they’ve already invested resources in it, such as time or money.

For instance, Mint users who spend a considerable amount of time and cognitive effort personalizing categories and budget configurations may feel emotionally invested in the app. This investment may prevent them from canceling their Mint account even if the service is no longer useful to them. In this manner, the Sunk Cost Fallacy reinforces the Status Quo Bias, which we discussed in the first article of this series, i.e. our natural inclination to stick with the status quo.

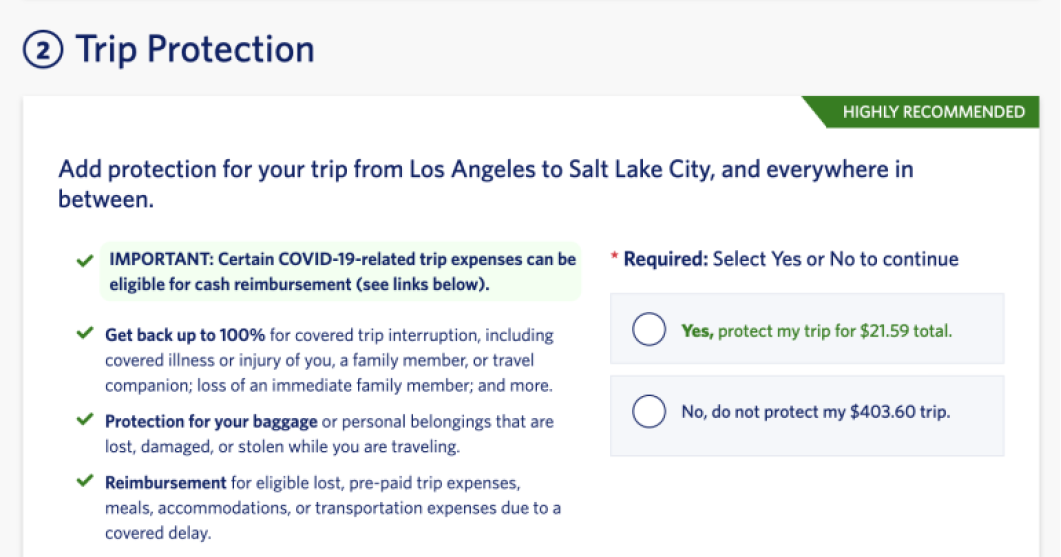

This bias is also evident in cases of embedded travel insurance. After allocating time and mental resources to plan travel logistics and secure flights, uninsured travelers are often inclined to opt for the readily available insurance options. This is despite that such options are usually more expensive, limited to a single trip, and superior alternatives might be just a click away.

To conclude, let’s review the case of Square’s free POS system. Entrepreneurs are initially drawn to it because of its pricing model that includes no upfront costs and is easy to understand. Additionally, there are no long-term commitments.

As businesses invest time and effort in embedding Square into their daily workflows, an emotional commitment develops. This commitment makes the idea of transitioning to, or even trying, another POS far less appealing. Here, both the Endowment Effect and Sunk Cost Fallacy come into play.

Crafting potent value propositions

As we have discovered today, embracing Loss Aversion as a lens for value perception, intertwined with Reference Point Dependence, empowers businesses to strategically refine their offerings. By understanding the reasons for customers inaction and reluctance, companies can craft potent value propositions that foster engagement, retention, and promote change.

In the next article, we’ll dive into the concept of Diminishing Sensitivity and explore how our perception of value diminishes as the magnitude of the outcome grows.

This article is the second of a three-part series grounded in Behavioral Economics, and more specifically, the Prospect Theory, where we explore how key behavioral biases are tied to value perception. Using fintech exemples, we showcase how understanding these biases can bolster value propositions, granting a marked competitive advantage.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of the Swiss FinTech Association.

Georgi Zai is a senior marketer with 20 years of experience in the financial and IT sectors, and an aspiring product manager. He has had impactful roles at Saxo Bank, UBS, and Falcon Bank, where he’s contributed to launching innovative financial products and applications.

Georgi Zai is a senior marketer with 20 years of experience in the financial and IT sectors, and an aspiring product manager. He has had impactful roles at Saxo Bank, UBS, and Falcon Bank, where he’s contributed to launching innovative financial products and applications.

Skilled both in strategy and execution, Georgi also brings a background in UX design, paired with a passion for behavioral science. He shares his expertise as a mentor to startups.

Outside the office, he’s an avid athlete and has completed 16 Ironmans, including the esteemed Ironman Hawaii.