The Swiss fintech monetas has established itself as a leader in for digital transaction systems. In our interview Vitus Ammann, monetas CMO, explains how the company got there and which struggles it had to overcome and how the technology will help with the democratization of finance.

You have made it into the top-100 fintech award and the Fintech 50, congratulations. How did you get there?

Vitus Ammann: It hasn’t been a small effort. We have had a group of investors from over 35 countries supporting us over three years to create a new type of platform that has the potential to redefine how not only transactions work, but the entire financial and settlement industry.

On your homepage you are modestly claiming that you are «developing [technology that] has the potential to revolutionize the global financial landscape». What is keeping the technology from achieving this goal right now?

Vitus Ammann «The result is the democratization of finance, much like the internet democratized communication.»

Today’s financial systems are built on top of antiquated centralized technology. Operational costs are prohibitively expensive. The result is that the current system has excluded over two billion people today who can’t participate in the global economy due to high distribution and replication costs. Cryptofinance technologies have the potential to lower costs to a level where the “long tail” (80% of the market) can finally be included. The result, is the democratization of finance, much like the internet democratized communication. The long-term benefits are unfathomable.

What does differentiate Monetas from other digital transaction systems – why will you prevail?

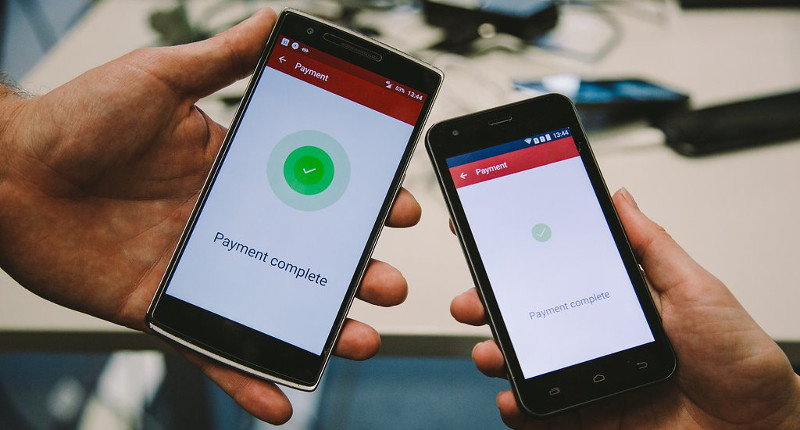

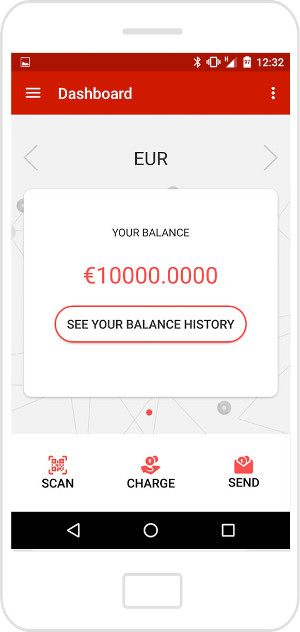

Monetas is different than every digital transaction system today because of one core feature – the absence of central account management. Every digital transaction system today requires the management of a central account. Today’s digital wallets are merely an access tool based upon the traditional legacy systems. When you look at your balance, you are actually looking at a representation of your balance that is recorded in a central ledger. With Monetas, the value is held on your device, and no 3rd party has the ability to modify this balance. A Monetas wallet is more similar to the wallet in your back pocket holding cash, than the e-banking application on your phone.

Monetas is different than every digital transaction system today because of one core feature – the absence of central account management. Every digital transaction system today requires the management of a central account. Today’s digital wallets are merely an access tool based upon the traditional legacy systems. When you look at your balance, you are actually looking at a representation of your balance that is recorded in a central ledger. With Monetas, the value is held on your device, and no 3rd party has the ability to modify this balance. A Monetas wallet is more similar to the wallet in your back pocket holding cash, than the e-banking application on your phone.

Monetas will prevail because it is the first truly global transaction platform. Sending value as a real time gross settlement allows for the ability to transact value like a WhatsApp message. Just like a WhatsApp message, it doesn’t matter where you are in the world.

It is difficult to compare Monetas to anything in existence because of the broad applications possible. Not only is Monetas a domestic payment solution comparable to M-Pesa in Kenya, it is also Western Union, a commodity and equity trading platform, a dynamic foreign exchange marketplace, and much more. Monetas makes settlements, reconciliation, and central account management obsolete thus reducing costs by an order of magnitude over legacy systems focused on single niche corridors.

What are your milestones this year…?

We are using 2016 to launch pilots in 12 African markets where we will be able to refine our product into a tool where language isn’t a requirement and people are able to use it intuitively. Importantly, we are working with our partners on regional specific integrations and customizations to ensure seamless national roll-outs.

… and where would you like to be in 5 years?

In five years, we believe the entire financial landscape will be changed. The difference will be going from 1995 to 2000 in the internet era. Once cryptofinance and blockchain technologies become the underlying drivers of financial platforms, we will see greater prosperity on earth as more people are able to access and use financial products that are designed to add stability to people’s lives. By 2021, Monetas will be active with partners worldwide. As Monetas licenses software to banks and financial service providers, anyone can go to their app store and download an application that allows them to send money to anyone on Earth for a fraction of the cost of what is possible today.

Could you give one concrete example of benefits that cryptotechnology brings to the world today and one of what it might bring in the future?

Although the possibilities are endless, let’s speculate what mass adoption of crypto-technology will look like. In emerging markets today, lending is incredibly difficult. People don’t have reliable credit scores, or risk profiles for lending. Financial institutions can’t afford to maintain relationships with, or loan to, individuals with little to no net wealth looking for a loan under $100. With cryptofinance, companies will be able to better generate risk profiles though analysis of a wide data set – from spending patterns and income per day, to social networks, location data and more. After a risk score is built if for individuals based on information gathered from nothing more than a smartphone, they will qualify for globally sourced crowed lending.

As a European, perhaps I want to avoid donating to mega-charities with high overhead and instead lend directly to whomever needs it. I will be able to choose the rate or interest I want back, as well as risk I am comfortable with. With only $10 to lend, I am able to diversify my risk by lending to $0.001 to 10,000 people who fit the parameters I chose. Because there is no financial intermediary, payments are sent directly. The repayment of the loan is automated, and based on smart-contracts that repay loans directly to the lender, wherever they are in the world. These sub 1 cent payments will open the door for entirely new business sectors, smart-metering for solar production, selling excess Wi-Fi from your phone, or acting as a spam filter to charge incoming emails $0.0001. Cryptofinance is in its infancy, just as the internet was in 1992. Although hard to fathom the full potential now, it is obvious to those in financial services that the future is cryptofinance.

Being a Swiss Start-Up, what are the pro and cons of being based in Switzerland?

Switzerland boasts a long tradition of privacy, direct democracy, respect for human rights, world-class infrastructure and educational institutions, and a stable, business-friendly legal and political system. It also has an exceptional level of expertise available in the areas of cryptography and security. The culture of stability has both its pros, and its cons. The cultural draw to stability attracts new graduates to long-term career-focused stability. In parallel, investors look for tangible, safe, and long-term investments that have already demonstrated success. Alternatively, Silicon Valley start-ups are full of young graduates who want to achieve the impossible while being backed by investors who are looking for nothing but the right idea to make it big.

If you could change one (structural) thing in the Swiss fintech landscape, what would it be? (e.g. less regulation, more engagement from city/state, tax benefits, …)

Monetas is focused on deploying software in markets around the world. Doing so requires subject matter experts and professionals with localized knowledge. The ability to hire diverse teams from many different countries and backgrounds and have them relocate to Switzerland easily would be a great benefit to growing such a globally focused company.

About Monetas: