Written by Therese Faessler.

Financial literacy is an important, wide, and encompassing concept with broad scope and great depth. In our first article, Why being financially literate is good for you, the economy, the country and society as a whole, we focused on the ripple effect of a financially literate individual within a family, which represents a household within a country and a participant(s) of an economy and in the end a member(s) of a society. In a second article we described the framework the components of financial literacy and why their order matters.

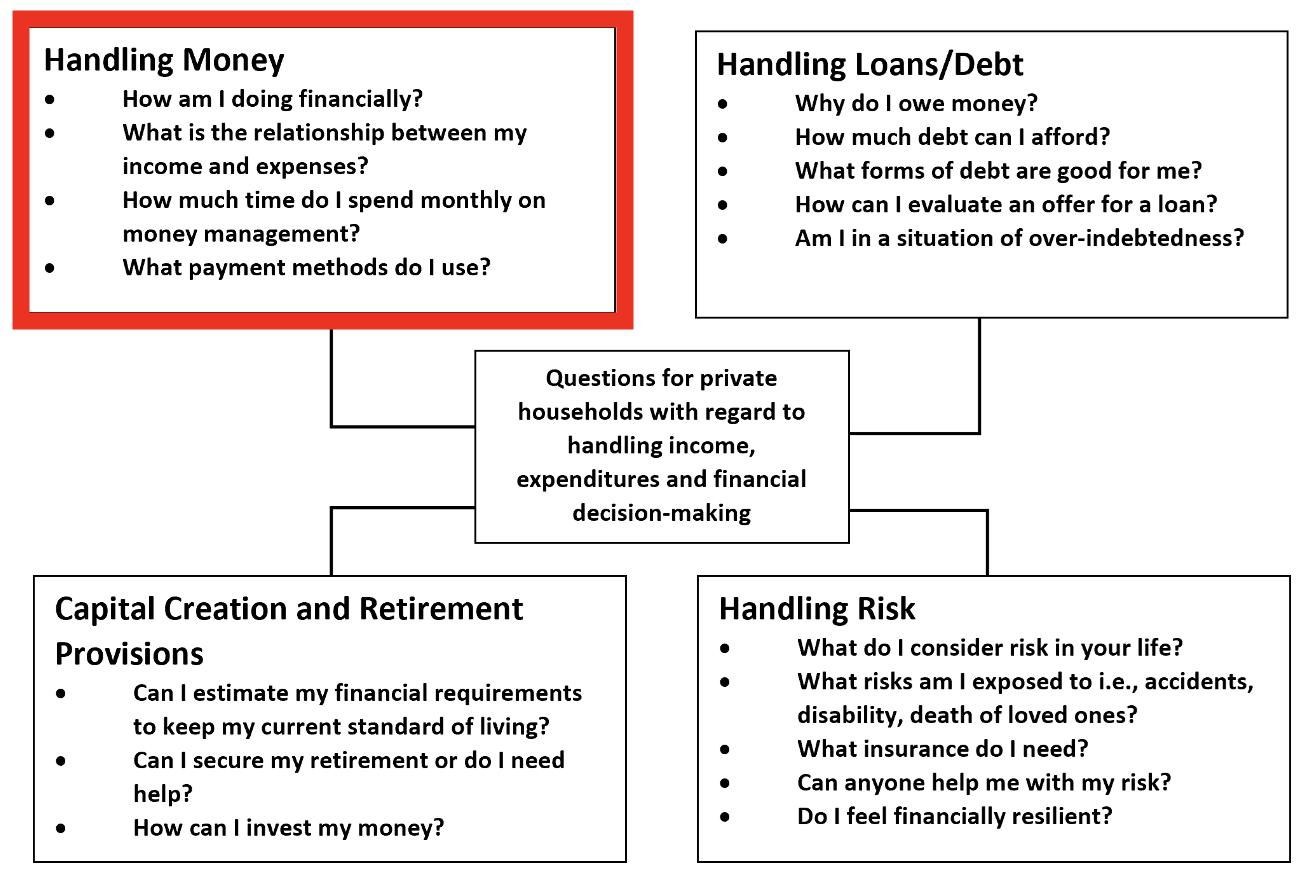

The Essential Quadrants of Financial Literacy

Most money coaches focus on debt management, budgeting, saving, and investing. However, we propose a different approach, categorizing these topics into budgeting & saving, debt management, insurance management, and wealth creation through investing. This reorganization makes wealth accumulation a clear, step-by-step process. The aim is to amass sufficient wealth during one’s working life to support themselves through retirement, using knowledge from these four quadrants.

Credits: Therese Faessler, invested.ch

Practice, Perseverance and Patience

Applying this knowledge effectively requires discipline. Knowledge alone is ineffective without the discipline to put it into practice, which involves persistence, patience, and the ability to replace bad habits with good ones. This is similar to adopting new health habits, like a balanced diet and regular exercise, which are widely recognized as beneficial but require consistent practice to be effective.

Handling Money is the Most Important Fundamental Quadrant

The fundamental aspect of financial literacy is handling money, which is based primarily on budgeting, or more specifically, saving. Budgeting involves strategizing how to allocate funds for spending and saving. Saving always comes first before spending. By assigning your money to your needs and wants every month, you can follow where it goes and you create an actionable plan where you spend less, by recognizing and reducing unnecessary expenses and consequently saving more for things you need and want in the future. There are 2 mantras for the budgeting and saving quadrant. The first one is from George S. Clason “Pay yourself first.” The second one is from Winston Churchill is “Failing to plan is planning to fail.” “Paying yourself first” is a refrain to remember and nudge oneself to save first and not last. Warren Buffett famously said, “Do not save what is left after spending, but spend what is left after saving.”

Everyone knows that learning a new skill without immediate gratification isn’t easy. There is no immediate reward. Learning to drive a car is fun because then you can jump in a car and go anywhere. That is immediate gratification. Budgeting is an investment in time, energy, and thought with a sacrifice, if “only” here and now. It is a matter of postponing purchases you’d like to make today. With a budget and “paying yourself first” as part of that budget you always plan to live within your financial means today and in the future. Basically while working and earning an income, living within your financial means is just spending less than you earn.

Credits Wallpaperflare

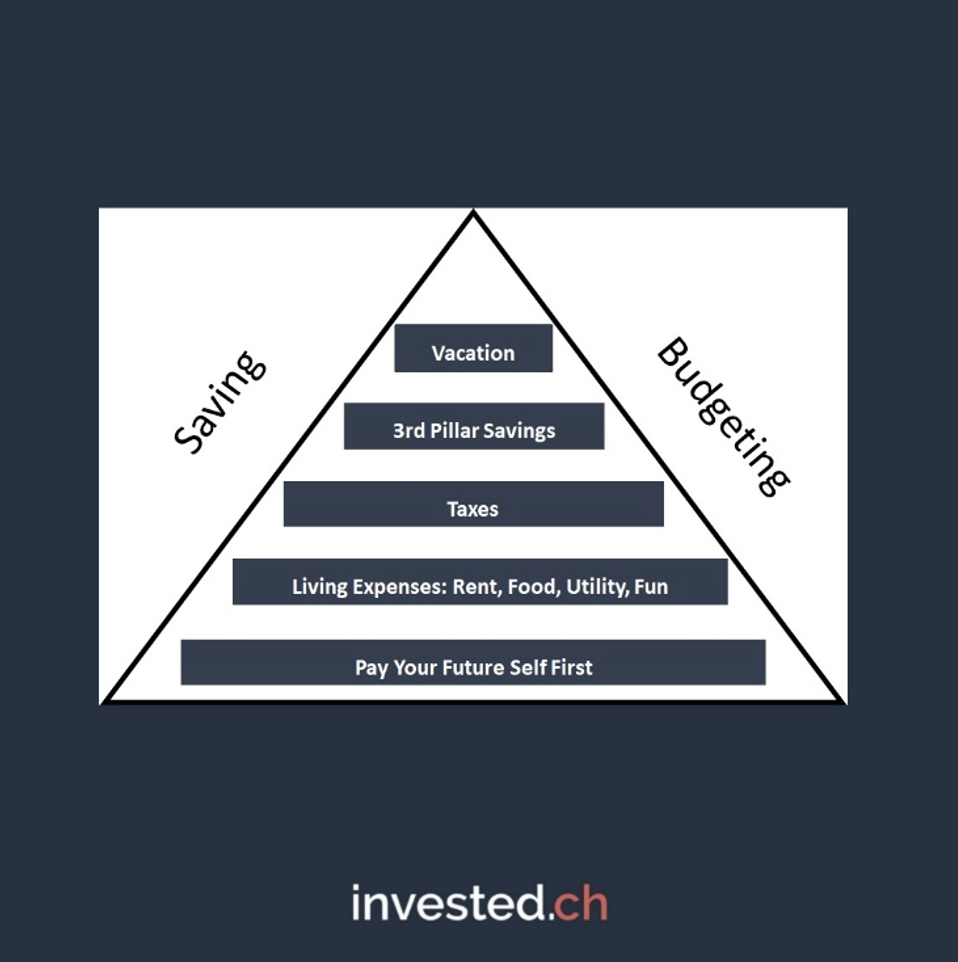

5 Things to Budget – Automatically

A comprehensive budget should include five key elements: First and foremost, some money must be set aside first for your future self and your own personal financial insurance fund, also known as your emergency fund. Secondly, everyone must pay their bills, that is rent, food and essentials, clothing, repayment of debt, insurance, etc. Thirdly, taxes are always a big percentage of a budget, so money for taxes must be set aside. Fourthly, it is good idea to save money in a tax deferred retirement account (saving on taxes). Fifth and always important, it is important to save for vacations. According to moneytransfers, a vacation on average for a family costs 1 month’s salary, around 8% of an annual income.

Money for your bills and taxes are clearly necessities to live. However, 3rd pillar or tax deferred savings are savings for retirement. They are listed here separately from “other savings” because there is an extra advantage to them. Most modern economies encourage their citizens to save for retirement by way of tax deferred savings accounts. This money in these savings accounts is usually blocked until retirement, but in order to incentivize citizens to save for their retirement, often governments don’t tax this as earned income. This money is usually taxed at a lesser rate when it is paid out.

Budgeting helps you in allocating money for short, medium, and long-term expenses, so that you can afford all three. Therefore, it is absolutely necessary for financial security and well-being. Building wealth by saving more and spending less will allow you to achieve the following:

- Achieve important goals, things like sending your children to good universities, paying off the mortgage on your home, and/or enjoying your retirement.

- Create an emergency fund to deal with unanticipated surprises, such as new roof or car repairs, illness, or unemployment. Most advisors would recommend about three to six months’ worth of income. However, it depends on how much one must maintain. Upkeep and the maintenance of a home is more expensive than the maintenance of an apartment.

- Exceptional expenditures for things you really want, such as a house, vacation or expensive new car.

- Save for retirement in a tax deferred interest-yielding bank account that not only keeps your money safe and out of reach, but also allows you to grow with better compound interest rates over time.

The Implementation – How to Make Saving an Inherent Ritual

You’ve heard all these ideas and “strategies” a million times before, but they really haven’t been appealing because YOLO … You Only Live Once and it is more fun right now to spend than to save. There are a few nudges that we’d like to give you here.

Think about the last raise you received from your employer. Was it 5% or 10% or maybe even 20%? How quickly did you “forget” that you received additional income? How quickly was it “just” spent? The same thing goes the other way around. If you have a bit less because you’ve automatically saved some of your income automatically, it quickly fades into the past and you get “used to” your new limits.

If you think saving is a hard new discipline or habit to practice, it is because it is. Behavioral economists like @der Entscheidungsarchitekt, Reto Blum, at Human Decision Design clarify the reasons it is hard, but also present some very useful tools as workarounds. Reto wrote from a behavioral economist’s point of view that there are four main reasons that people don’t save and budget in spite of knowing that they should.

- We have a cognitive overload – Our cognitive capacity is limited and thus with too much information, we are quickly overwhelmed.

- We have a present focus bias – We have been conditioned to focus on the here and now as a part of our survival instinct.

- There exists cognitive fatigue – Patience and discipline are struggles. The more challenges we face the less patience and discipline we have for any new undertaking.

- We view the world with a hyperbolic discounting of the future. – We value the present over the future.

And my take …

- We have a limited amount of time – We value the time spent on working, family, and relaxing over the time required for future financial wellbeing maintenance.

So what are the workarounds?

- Automatic deposit –

- Cognitive overload

With so many decisions to make everyday from when to get up to when to go to bed, automatically depositing a fraction of your salary alleviates the energy required to make a decision and then act on it. - Time constraints

Setting up the automatic deposit requires a fraction of the time of making manual deposits with each salary. It is easier, more efficient, and more effective. - Present focus bias

By automatically depositing money, you can trick your bias by not actually acknowledging it.

- Cognitive overload

- Commitment device

Commitment Devices have two main features.

With this device you make voluntary decision now that defines your choices in the future. The goal of a commitment device is to align future choices to your long-term goals. Daniel Goldstein, the famed behavioral economist, described the goal of these devices as making decisions with a ’cool head’ (now) to bind yourself so that you don’t make spontaneous bad decisions (in the future).-

- You must understand the gaps exist between your intention and your actions.

- Commitment devices triggers a cost when you do not act as with your stated intentions and goals.

- Cognitive overload

Predefined choices leave no option for thought. A new option is expensive. - Cognitive fatigue

Predefined choices are default choices, they cost no energy.

-

- Commitment community

Instead of a device, a community like Alcoholics Anonymous can help in commiting to long run decisions. Just like the devices the community holds you to your predefined choices by way of peer pressure.- Cognitive overload

Predefined choices leave no option for thought. A new option is expensive. - Cognative fatigue

Predefined choices are default choices, they cost no energy. - Time constaints

Combining social interaction with trusted communities who act as commitment devices allows you to enjoy social interaction while holding on to your commitments. - Hyperbolic discounting of future

Your community will remind you of the value of your decisions without questioning the commitments you made with a “cool head.”

- Cognitive overload

In Summation

- If you haven’t started saving regularly and rigorously, don’t worry, you are not alone.

- If you find it hard to start saving the way you know you should, don’t fret, it’s not easy.

- There are tools and methods to make saving easier or at least less painful.

Introduction to the next article

In our next article we will concentrate on debt. How much debt can afford? What types of debt are there? What are the interest rates and how do they differ to the annual interest rates?

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of the Swiss FinTech Association.

Therese Faessler is an active member of the Swiss FinTech Association and serves as Head of Financial Literacy.

She is a strong, global proponent of Financial Literacy and works as an associate at the Swiss National Bank’s educational program. Her goal is to increase financial literacy in individuals as to trigger the ripples and shrink wealth gaps.

She manages a website, invested.ch, which she uses to teach financial literacy at Swiss high schools.