Written by Therese Faessler.

Financial literacy is an important, wide, and encompassing concept with broad scope and great depth. In our first article, Why being financially literate is good for you, the economy, the country …, we focused on the ripple effect of a financially literate individual within a family, which represents a household within a country and a participant(s) of an economy and in the end a member(s) of a society. In this second article we describe the framework and the components of financial literacy and why their order matters.

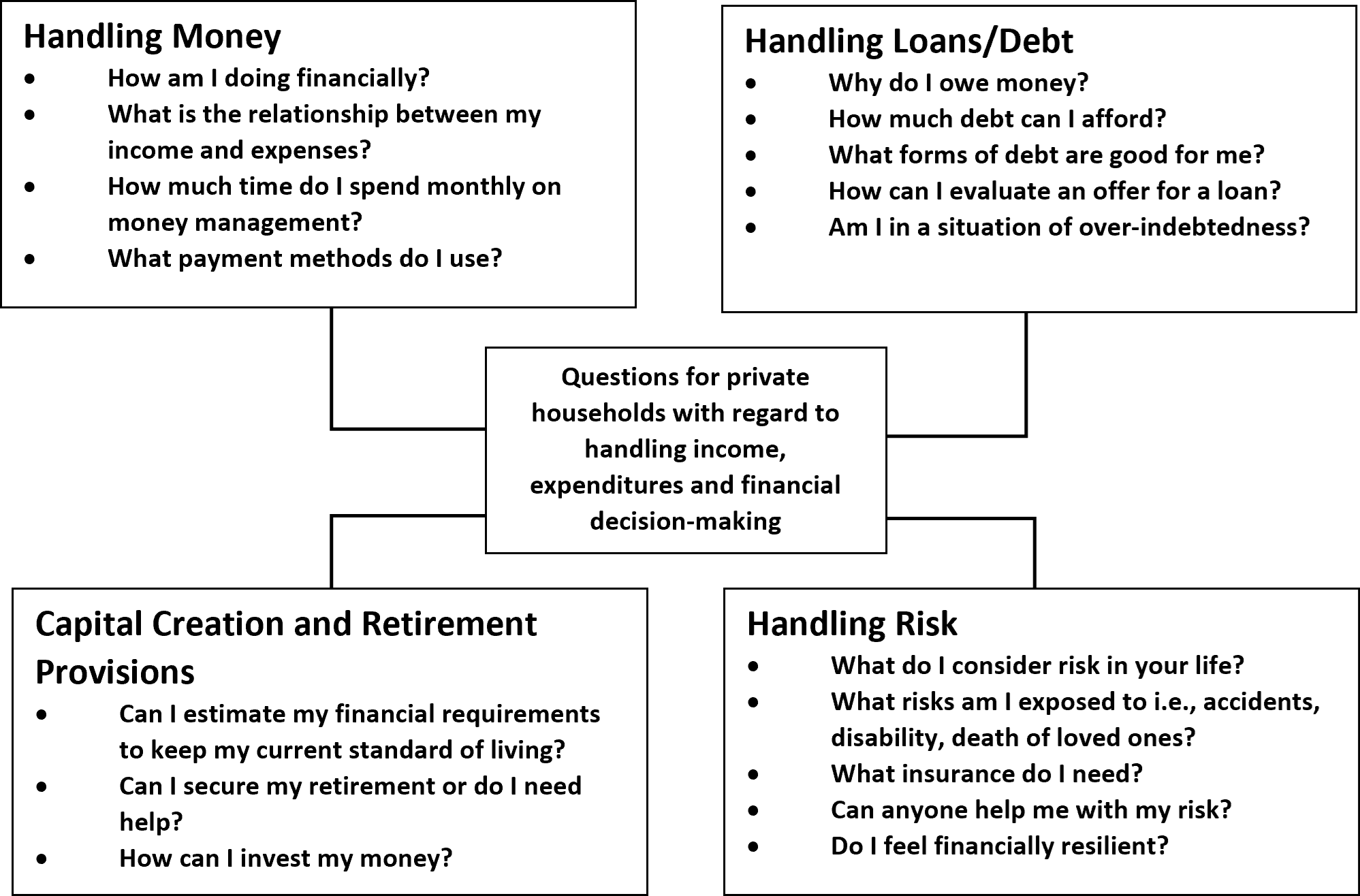

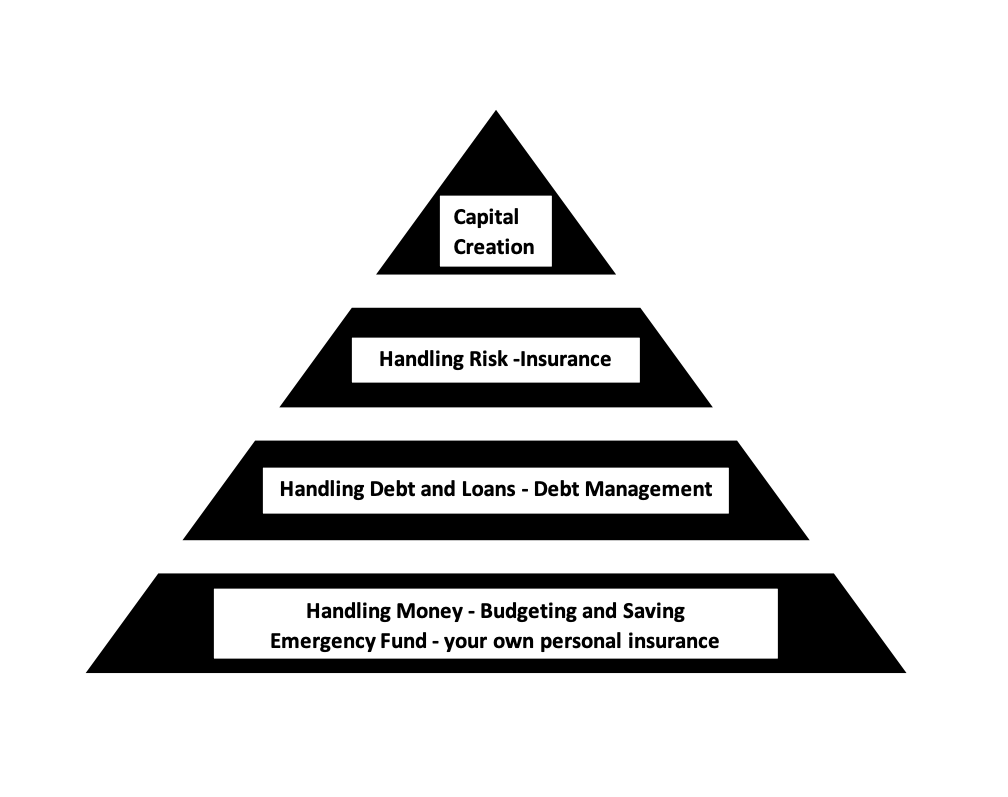

The Essential Quadrants of Financial Literacy

Most educators talk about debt, budgeting, saving, and investing. Here we redefine those core topics as budgeting & saving, managing debt, insuring, and investing (creating wealth). With this new bundling, the accumulation of wealth becomes a step-by-step curriculum and process. The ultimate goal is to build enough wealth throughout a working lifetime to last a whole lifetime by applying the knowledge gained from each of these quadrants.

Credits Therese Faessler

Applying knowledge more explicitly means practicing discipline. Although knowledge is essential, without the discipline, namely practice, perseverance and patience, the knowledge is useless. Discipline is also about “unlearning” bad habits and replacing them with good habits. Practicing financial literacy fundamentals is like practicing healthy habits. It is not enough to know that a body fairs better over time with a healthy diet, healthy habits, and exercise. Without integrating healthy habits as with financially responsible habits, the benefit of the knowledge is nonexistent.

Handling Money

Handling Money is about budgeting and saving. Budgeting and saving are the first and crucial fundamental components of financial well-being. Budgeting is the learned and practiced skill of planning and managing your money. By allocating your money every month, you can follow how it flows and you can create an actionable plan by which you can spend less, by reducing unnecessary expenses and saving more for the things you need and want in the future. There are 2 mantras for the budgeting and saving quadrant. The first one from Winston Churchill is ”Failing to plan is planning to fail.” And the second one is from George S. Clason “Pay yourself first.” Basically, “paying yourself first” is a mantra to motivate, encourage, incentivize, and nudge oneself to save first and not last. Warren Buffett famously said, “Do not save what is left after spending, but spend what is left after saving”.

Credits Wallpaperflare

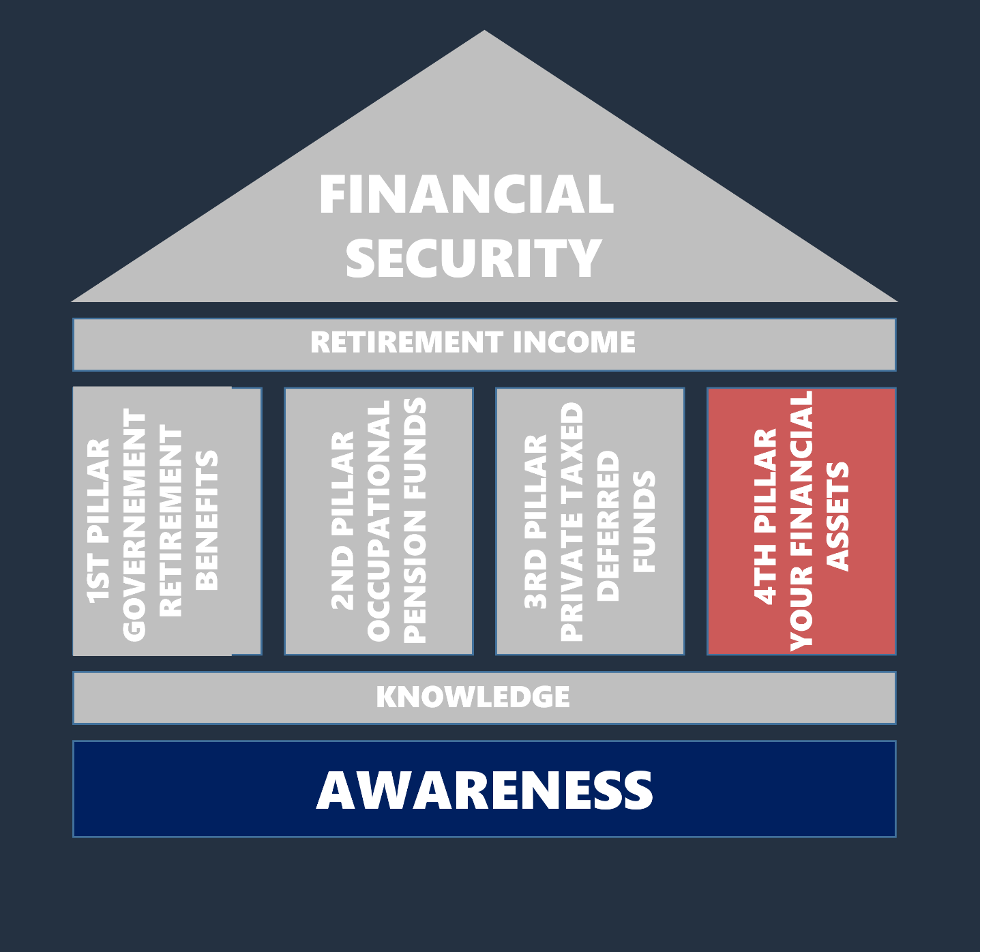

With a budget and having “paid yourself first” as part of the budget you always plan to live within your financial means today and in the future. Living within your financial means is a matter of allocating so much less to spending than you earn. In a budget there are basically 5 things to think about. Everyone has to pay their bills, that is rent, food, clothing, repayment of debt, health insurance, etc. Taxes are always a big chunk of a budget, so money for that has to be set aside too. It is not a bad idea to put money in a tax deferred retirement account. The main reason for this account is to save taxes. Most modern economies have these tax deferred savings accounts to encourage citizens to save for their retirement. This money is usually blocked until retirement, but to incentivize citizens to save for retirement, often governments don’t tax this as earned income when it is earned. Money must also be set aside for vacation. Vacation is also an expense that should be planned and budgeted. According to moneytransfers.com an average vacation for an average family of 4 is equal to about one month’s salary or 8% of an annual income. Last but not least, it is of utmost importance to have an emergency fund.

Budgeting helps you plan for short, medium, and long-term expenses, enabling you to save accordingly to afford all three. It is, therefore, entirely necessary for financial security and independence. Wealth is built through spending less of your income so that you can achieve the following:

- Realize important goals, things like sending children to a good university, paying off the mortgage on your home, and/or enjoying your retirement.

- Establish an emergency fund to cope with life’s unexpected surprises, such as roof or car repairs, illness, or a spell of unemployment. This should be about three to six months’ worth of income depending on how much one has to maintain. Maintaining a home is more expensive than maintaining an apartment.

- Extraordinary expenditures for things you really want, such as a vacation or new car.

- Saving for your retirement in a tax deferred interest-yielding bank account that not only keeps your money safe and out of reach, but also allows you to grow it over time with better interest rates.

Handling Debt and Loans

Handling debt and loans is a cornerstone of financial literacy because if left uncontrolled it can take over full control of one’s financial well-being. Debt is money owed to someone or an institution. Debt is used to make large purchases that in a current situation are not financially possible. Debt must usually be paid back with added interest. For debt the key takeaway is that like compound interest on a savings account, debt also accrues in value. This means that the interest on the debt owed is subject to interest too. There is always an interest rate on debt. Not paying off the debt at the set date means the debt will be greater by the amount of interest owed. This greater debt is subject to interest too. So, debt grows exponentially with the interest rate. Just as a teaser for the blog post on debt, Forbes reported on November 13th, 2023, that the average annual interest rate on a credit card is 27.80%.

Handling risk

Insurance is a way to mitigate risk. A car insurance policy protects your financial investment in your car as well as if you are at fault, your responsibility for harming others. Health insurance limits your liability in case of illness or accident. Homeowners insurance covers damage to your home, property, personal belongings, and other assets in your home. Having insurance is the best way to manage your chance of losses due to living a normal life.

So now you’ve budgeted and thereby saved. You’ve managed your debt with ease. You have the insurance you need in place to create financial stability without any shocks. Now it is time to prepare for your future without an income.

Credits Gstudioimagen1

Capital Creation and Retirement Provisions

Capital Creation always includes investments. The reason for this is that there are only 24 hours in a day and only 7 days in a week. That means creating capital by working harder or more is strictly limited. With inflation, or the increase in goods and services prices, cash loses its value as long as it is parked, whether in a bank account or under a mattress. The good news is that you can make your money work for you. By investing in things that become more valuable over time, makes your investments more valuable too. Those things can be, for example, real estate, property, metals, funds, or stocks. By using an investment that can incorporate a compound interest, your wealth can grow exponentially. How to integrate a compound interest in your investments will be discussed in greater detail in the last blog on Capital Creation.

Credits Therese Faessler

The order of the quadrants matters!

Financial well-being all starts with an income. That income must be budgeted and planned. It must be divvied up into pieces that make living on one’s own income sustainable. Here sustainable means having a sufficient amount of financial resources for a lifetime. A portion of that income must be set aside for bills including taxes, the furniture store for the kitchen table, the grocery store for daily needs, the rent to the landlord, etc. Another portion, and this is very important, will go to paying off debt so that it doesn’t accumulate with interest exponentially. Another portion of that income will go to insurance so that if there is an illness, robbery or accident, the wealth you’ve accumulated thus far, is insured (like for your car or jewelry).

Credits Therese Faessler

Thus, the order matters because with an income, there is a plan to budget and save. With that budget, savings are made, expenses are paid, debt is paid off and insurance is bought to stave off the uncertainties of life. After having planned (“Failing to plan is planning to fail) and saved (“Pay yourself first”), what is left over should be invested to avoid the risk of inflation.

In other words, financial literacy is a tool to manage an uncertain financial future. Life is risky. Being prepared is the only way to manage risk. Start with an income and budget and save for the risk of living. Make sure you take advantage of experts calculating risk, namely have insurance. Plan to pay off debt so that it doesn’t grow exponentially with interest. Finally, when all the financial risks to today are covered including your own personal emergency fund, start building your own retirement fund for the time when there is no salary, when you are retired. Nota bene: The savings in your bank account that you don’t need in the next 6 months will be worth less next year. And you cannot invest with the money you need tomorrow. The order of the financial literacy quadrants matter! Inflation eats up savings and investments take time.

In our next article we will concentrate of how to budget and save, their importance and why “Failing to plan is planning to fail.” Living paycheck to paycheck is a self-imposed budget because no one wants to accumulate debt inadvertently.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of the Swiss FinTech Association.

Therese Faessler is an active member of the Swiss FinTech Association and serves as Head of Financial Literacy.

She is a strong, global proponent of Financial Literacy and works as an associate at the Swiss National Bank’s educational program. Her goal is to increase financial literacy in individuals as to trigger the ripples and shrink wealth gaps.

She manages a website, invested.ch, which she uses to teach financial literacy at Swiss high schools.