In my first post, I wrote about how we are constantly hearing buzz around the ‘war being over’ between FinTechs and banks. The case for symbiosis and coopetition over competition between the Davids and Goliaths is certainly strong; so strong that 82% of banks, insurers, and asset managers are planning on increasing FinTech partnerships over the next three years (PwC, 2017). That said, I also questioned the success of FinTech-bank partnerships in delivering true value for the bank, the start-up, and/or the customer.

In my first post, I wrote about how we are constantly hearing buzz around the ‘war being over’ between FinTechs and banks. The case for symbiosis and coopetition over competition between the Davids and Goliaths is certainly strong; so strong that 82% of banks, insurers, and asset managers are planning on increasing FinTech partnerships over the next three years (PwC, 2017). That said, I also questioned the success of FinTech-bank partnerships in delivering true value for the bank, the start-up, and/or the customer.

There is no denying that there have been some highly successful partnerships to date. However, there is also no hiding from the fact that many of the ‘partnerships’ we hear about have been used to drive marketing and PR efforts while many have simply not delivered the intended value and have been brushed under the carpet.

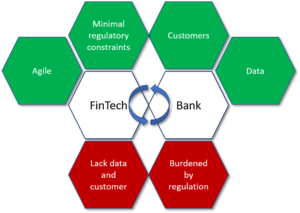

The inconsistency of success stories is to be expected in a market which is undergoing such profound changes in terms of structure and objectives. It is also to be expected given the vast differences in culture and organizational structures between the banks and FinTechs. On the one hand, incumbent banks with access to vast customer bases and related data are weighed down by regulation and organization size. On the other hand, FinTech start-ups, built upon the promise of being nimble enough to respond quickly to market trends, have minimal regulatory constraints, but lack in customers and data. As these entities continue to cooperate, shared understandings regarding each’s abilities are being established and adaptation is underway.

The adaptation is twofold. For FinTechs, they are beginning to realize how cumbersome regulation in the banking sector is, and how this impacts the rate of change. Adapting to this is not easy, especially when longer than usual sales cycles can put a heavy strain on the cashflow supporting new ventures. Understanding the time to production and forecasting accordingly is crucial for a FinTech’s survival and the development of its partner relations as it removes the need for excessive calls to bank-side innovation managers, a key pain point recognized throughout banks.

For banks, they are understanding that digital evolution (or revolution) cannot happen if business and IT structures remain siloed. The two sides need to better understand how to integrate and work together; an understanding that would be facilitated by increasing the number of board directors with technical backgrounds. Similarly, the procurement process remains a key area of contention as partner onboarding processes that have not responded to a market increasingly dominated by emergent service and solution providers. Asking a two year old company for a detailed list of references or three years of accounts is clearly going to slow down the partnership process, frustrating both parties in the meantime.

These teething problems, coupled with the uncertainty that the digital revolution has created, is a reason that many partnerships have, to date, been relatively unambitious and targeted at specific problems (e.g. AML, KYC, customer service etc.) The core banking system remains intact and is far from being disrupted; many entrepreneurs who originally set out to disrupt are revising their strategies. As a result, the change and innovation that these partnerships are trying to achieve is largely incremental as both parties navigate their differing realities.

While this is the status quo, the eco-system is in constant change, shifting and tweaking to perfect itself, learn from past errors, and increase the delivered value. The changing nature of and the steady increase in partnerships is allowing both parties to better understand each other and adapt to their respective differences, streamlining the process from both ends.

The partnership approach has been more complicated than originally anticipated and both entities in the partnerships need to get better at working together. There is also an increasing role for intermediaries, consultants, and brokers to support and guide both parties culturally and technically. However, with more to lose, if incumbent banks do not learn how to better collaborate, restructure, and become more agile, the threat of digital-only challenger banks (e.g. Monzo and N26) will only grow.

– Text by Charles Burns

Charles Burns is Business Developer and FinTech Scout for AlmavivA, the largest Italian systems integrator. He works with leading FinTech’s and Italian financial institutions, promoting partnerships and commercialization of new products and services. Prior to joining AlmavivA he spent four years in strategy consulting at KAE in London. He holds and MBA from Copenhagen Business School.